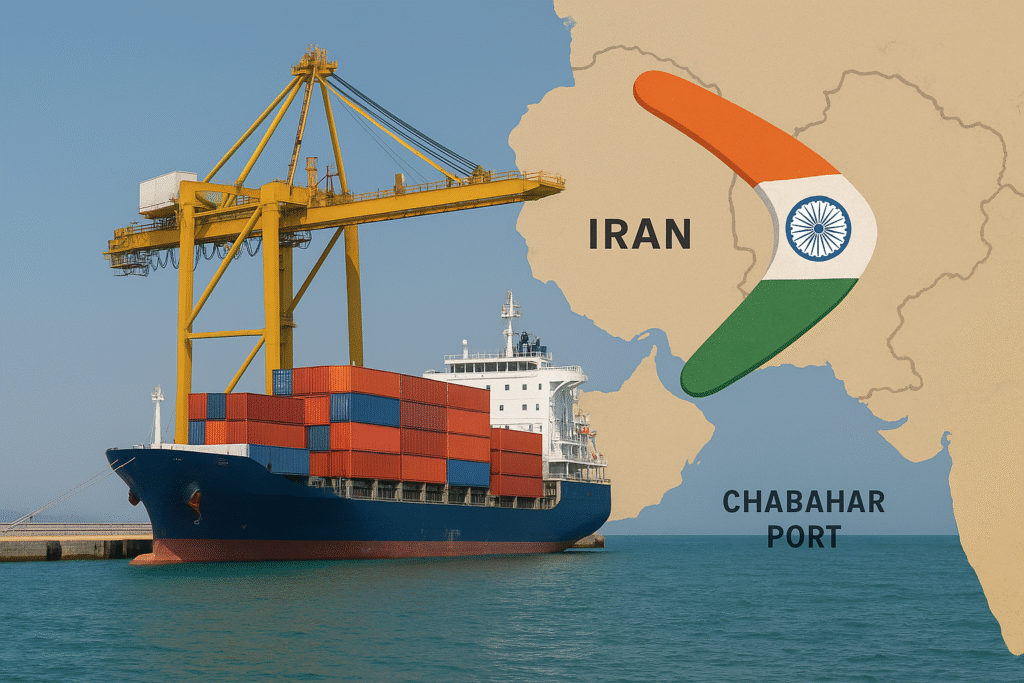

India’s Strategic Bet at Chabahar Port

On paper, Chabahar port was India’s “peaceful connectivity.” The strategic intent was to bypass Pakistan’s ports, marginalise Karachi and Gwadar, and cultivate leverage in Kabul and beyond. That calculus has met hard law and harder finance. The problem for India is now unambiguous. With United Nations (UN) sanctions “snapback” on Iran effective 27 September 2025 and the European Union (EU) re-imposing all nuclear-related measures on 29 September, the compliance tide has turned. As the United States (US) warned that “anyone considering business deals with Iran” faces “potential risk of sanctions,” India’s bet has swung back like a boomerang.

New Delhi’s operational bet was India Ports Global Limited (IPGL), which inked a 10-year operating deal at Chabahar port’s Shahid Beheshti terminal, celebrated in May 2024. The deal was marketed as India’s route to Eurasia without touching Pakistani territory. Even then, the US publicly warned, but New Delhi pressed on. Now the waiver umbrella is gone, and the project sits in a sanction’s crossfire. The “connectivity” narrative cannot outrun the compliance reality. This is the crux of India’s miscalculation.

The numbers never favored the Indian narrative. Indian outlets spoke of a decade-long ramp to roughly half a million twenty-foot equivalent units (TEU), and of a USD 370 million investment envelope. Those targets were fragile even before snapback; they become speculative when premium pricing and coverage uncertainty deter carriers. Another Indian report puts cumulative cargo handled at over 8 million tonnes since IPGL’s involvement, hardly transformative for a project long cast as a Eurasian pivot.

Indian voices now sound defensive and divided. Ministry of External Affairs (MEA) spokesperson Randhir Jaiswal said India is “examining the implications,” signalling sanctions-driven risk to payments, insurance, and carriers. Congress leader Shashi Tharoor publicly questioned the diaspora’s silence as policy setbacks, such as Chabahar port’s waiver’s end pile up. Inside the system, IPGL directors reportedly resigned as exposure rose, underscoring operational strain rather than “strategic autonomy.”

By contrast, Pakistan’s position in 2025 is stronger on facts, not slogans. Karachi Port Trust (KPT) closed FY2024/25 with a record 54 million tones and 2.65 million TEU. These verified figures reflect operational depth and policy continuity. Port Qasim Authority (PQA) continues to complement KPT with industrial cargoes, while deep-sea Gwadar port, though smaller, retains strategic headroom. Pakistan will also leverage trade-route to the Central Asian Republics (CARs) by further developing it. These are functioning assets with established connectivity into “hinterland” markets.

Equally important is corridor diplomacy. The Uzbekistan-Afghanistan-Pakistan (UAP) railway agreement signed in July 2025 re-anchors Central Asian access to the Arabian Sea through Pakistan. Current estimates put the cost near USD 7 billion, with a planned route of about 700 km through Afghanistan. Credible assessments expect transit times from Uzbekistan to Pakistan to fall from roughly 35 days to 3-5 days and throughput to scale towards 20 million tones annually after commissioning. None of this requires a sanction carve-out. All it needs is predictable compliance by the three states and a favorable geography.

To achieve this success, Pakistan’s diplomatic method has been incremental rather than theatrical. Given the current environment, two near-term policies are obvious. First, blend financing for UAP from Central Asian, Gulf and multilateral windows to reduce concentration risk. Second, China, Pakistan, and Afghanistan have reaffirmed extending China-Pakistan Economic Corridor (CPEC) into Afghanistan. As it works out, Pakistan can market a logistics package for Central Asian shippers that guarantees predictable clearance and port performance at KPT and PQA. By these successes, Pakistan’s geo-economics appeal will surpass any future “geostrategic venture” from India.

The strategic contrast is obvious. India sought to castigate Pakistan through detour geopolitics. Its strategy was to use Chabahar port to reduce Pakistan’s centrality, oust Gwadar, and thus give leverage to New Delhi in Afghanistan. However, the sanctions have had a counter-productive effect. The Indian entities now face a 45-day exit window in Chabahar port. The trade volume between India and CARs is around USD 1.7-2 billion, for which India will have to spend an extra USD 500 million to execute the trade through Gulf ports or mixed air/land routes while facing payment clearance, ship insurance and delaying issues.

In sum, Chabahar port has delivered India a boomerang, not a breakthrough. The wager on bypassing Pakistan has been repriced by sanctions, insurance, and carrier risk. On the other hand, Pakistan’s shorter corridors, higher throughput, and steadier diplomacy now anchor the workable path to the sea for Central Asia. Islamabad retains the sea strength grounded in geography and regulatory compliance, as Nicholas Spykman counselled, “Who controls the Rimland rules Eurasia, who rules Eurasia controls the destinies of the world.” Pakistan sits at the hinge of the Rimland position and thus provides reliability where India has only offered narrative.